Table of Contents

Going into residency can mean moving across the country, changing your financial habits, balancing residency and settling into a new home.

Setting up a budget during this time can help bring calm to the chaos. It enables you to better grasp where your money is going and provides you with a better overall financial picture.

There are simple ways to set up your budget so it’s easy to track and not a burden!

How Do I Budget?

First, you will want to determine your monthly income and then list all your monthly expenses. Then, decide how you want to intentionally allocate the money left over. This is the money you usually allocate to things like shopping, spending, leisure, and “self-care” and going out or dining out.

There are many budgeting methods out there that you can try.

The pay-yourself-first budget is where you allocate money to your savings each month first before any other expenses.

The cash envelope system is where you set aside your money by placing your cash in physical envelopes designated for each expense. This gives you a way of visually and tangibly taking control of your money.

Another method is the zero-based budget. The budget is calculated by taking your total income and allocating every dollar to an “expense.” Expenses could include bills, savings, emergency funds, groceries, entertainment, etc. By allocating all of your income somewhere, every dollar has a purpose, and you avoid spending on a whim.

You can choose any budgeting method you would like; the important thing is just sticking to it!

To keep it simple, you could follow a simple budgeting framework.

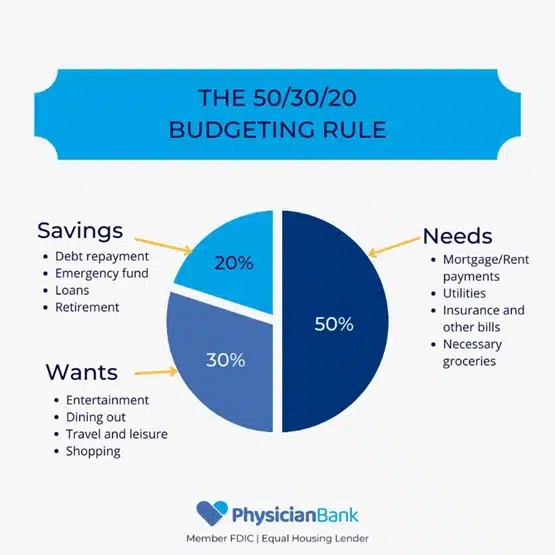

One common budgeting framework is called the 50/30/20 rule. This means 50% of your monthly budget should go toward needs, 30% towards wants, and 20% toward savings and paying off debt.

Your needs should include basic utilities, housing, transportation, insurance, loan payments, childcare, and other necessary expenses.

The wants should include things like entertainment and dining out. Last, savings should include any savings, emergency funds, and debt repayment.

Automate Your Bill Pay

Set up monthly autopayments for your utilities and other bills. Have your bills taken out of your paycheck right away instead of waiting for the due date so you can ensure your bills are taken care of before spending on other things.

For your utilities, you can usually set up autopayments with utility vendors. You can set the amount and date, and which account you’d like the money to come out of. This way, you will also never have late payments on your credit report or have to pay pesky late fees.

Set Up Autopayments or Direct Deposits to Your Savings

By having some “set it and forget it” contributions to your savings, you’re more likely to build up your savings without having to manually add money to your savings every so often.

You should be able to set up auto payments to your savings account from your checking account. This will pull an amount each month like you’re paying a bill.

For direct deposit, usually you can set up a percentage of your direct deposit to go to your savings account, and the rest to your checking. So, when you get paid, you add to your savings instantly! Check with your HR or payroll team to see if your company allows you to split your direct deposit between multiple accounts.

Use an App to Manage and Track Your Financial Standings

In our Physician Bank digital banking app, you can set and track your budget and financial goals.

You can also use our app’s myMoney feature, which has several budget-friendly functions.

- Analyzing spending by category. You can see an overview of your spending by category, like dining out, health, fees, and more. This way, you can easily recognize if you are overspending in a certain area.

- Budgets: you can add budgets with tags for various categories, including clothing, groceries, payments, and education. You can also choose which account to apply your budget and set up alerts for when you reach your budget.

- Goals. Set goals like “pay off student loans” or “save for buying a house” and set up monthly payments or a completion date to get motivated to save!

Create a Spending Plan

Focus on needs over wants. Allocate money for essentials like rent, groceries, and transportation before leisure.

Plan for Loan Repayments

Consider deferment or income-driven repayment plans if loan payments are overwhelming during residency.

Avoid Lifestyle Inflation

Just because you earn more as you progress does not mean your expenses should rise simultaneously.

Build Credit Wisely

Pay your credit card bills on time and in full to establish good credit without accruing debt.

Plan for Big Expenses

Know when major purchases like exams or buying a house are coming and start saving for them early.

Happy Budgeting

As you embark on your residency journey, it is essential to cultivate strong financial habits that will serve you now and in the future. Following a budget may sound daunting, but once established, it can offer peace of mind as you track your spending and see your progress toward financial goals. Be diligent about monitoring your expenses, avoid unnecessary overspending, and make informed financial choices. Remember, while professional development is crucial, financial well-being is equally important. Don’t overlook the importance of enjoying this transformative experience, prioritizing self-care, and wishing you the best of luck in your residency!

Are you a physician in need of a loan or new banking experience? Physician Bank was made for you!

Start a conversation with us today.

Are you a physician in need of a loan? Physician Bank was made for you!

Start a conversation with us today.

Comments are closed