Table of Contents

Pursuing a medical career involves years of study, residency, and a strong desire to establish roots in a new community. Your aspirations of finding the ideal home are not just tangible; they are achievable, especially with the right information about physician loans that are customized to suit your specific financial situation. This guide will assist medical residents in the smooth transition from residency to homeownership, offering valuable insights into specialized mortgage solutions that are tailored to meet the unique requirements of healthcare professionals like yourself.

Understanding Resident Physician Loans

Conventional mortgages might seem impossible when the weight of student loans and the starting salary as a resident physician are combined. This is where physician loans come in, unaffected by the typical down payment and income verification requirements. What’s in it for you? A smoother path to owning your dream home with more favorable terms. These loan programs understand the delayed financial trajectory of medical professionals and work to provide relief in the form of lower down payments, often as low as zero percent, and flexible repayment structures.

Why Physician Loans Make Sense

One of the main reasons physician home loans exist is because of doctors’ unique financial situation. These home loans are designed to help residents with no private mortgage insurance (PMI) requirements, less stringent down payment necessities, and the ability to close on the loan before securing your first full-time job as an attending physician are just a few benefits that speak directly to your situation.

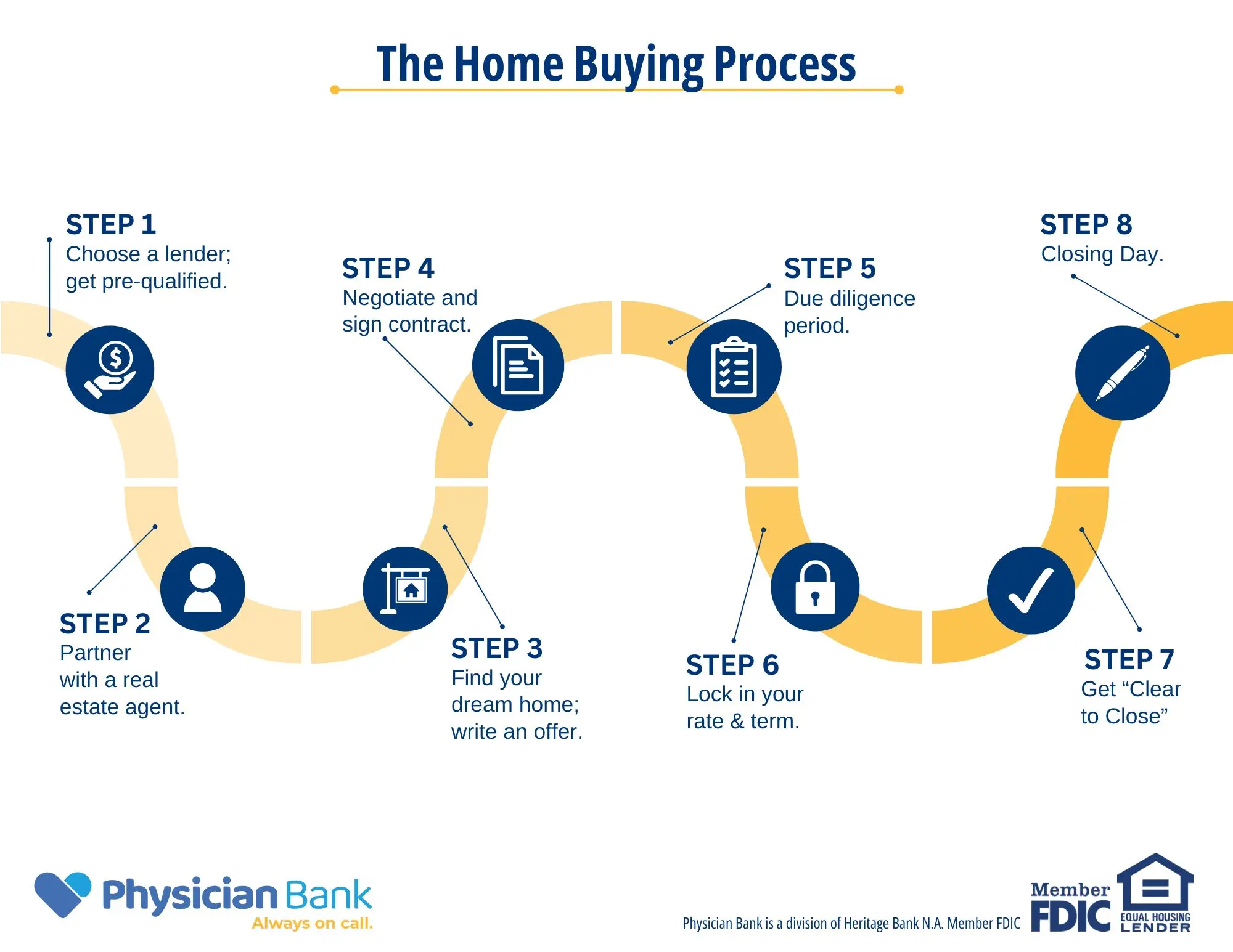

Qualifying for a Physician Loan: What Residents Need to Know

To start the homebuying process, ensure you meet the eligibility criteria for physician home loans. Here’s a walkthrough of what we typically look for and what you can expect.

Get A Customized Resident Physician Home Loan Plan

By partnering with a lender experienced in physician loans, you can secure a plan that meets your immediate needs and aligns with your long-term financial goals. This personalized plan considers factors such as your student loan debt, potential for future income growth, and the unique challenges faced by medical professionals entering the housing market. With a customized physician home loan plan, you are not simply finding a lender but rather establishing a relationship with a lender who comprehends the intricacies of your profession.

Find Expert Advice Tailored to Residents

Seeking expert advice tailored specifically to medical professionals is crucial when navigating home-buying. Financial advisors and mortgage lenders with experience serving doctors can offer invaluable insights into structuring your home purchase. They understand the unique financial pressures, including student loans and residency contracts, which can significantly impact your buying power. These professionals can guide you through selecting the best physician loan program that caters to your specific needs, providing clarity on terms, interest rates, and repayment schedules.

Will Student Loan Debt Affect My Qualifications?

Due to their extensive education, lenders understand that medical professionals often carry significant student loan debt. However, having this debt does not automatically disqualify you from securing a home loan. In fact, many lenders have specific provisions for calculating debt-to-income (DTI) ratios that are more favorable for physicians.

Take the First Step

Reach out to the Physician Bank team to better understand our physician loan programs, receive guidance, and to get personalized service that aligns with your career’s guiding principles.

Matt Velline

Matt Velline is a highly experienced lending expert with over 20 years’ experience in the mortgage and real estate industry. He has been with Heritage Bank and its subsidiary, Physician Bank, for over two years. In addition to his work in lending, Matt is also a professional musician who tours internationally. He prioritizes both his family life and the pursuit of personal prosperity.

What sets Matt apart from other loan officers is his real estate experience. As a licensed real estate agent, he takes a comprehensive approach to home-buying. This allows him to better relate to and advise his customers throughout their purchasing journey.

Comments are closed