Table of Contents

When you’re applying for a physician home loan, Physician Bank is going to want to know that you can afford the monthly payments. One way they do this is by looking at your debt-to-income ratio. This number tells us how much of your income goes towards debt payments each month. In this article, we will discuss what debt-to-income ratio is and how to calculate it. We’ll also give you some tips on how to improve your ratio so you can get approved for that Physician mortgage loan!

Debt-to-income ratio, or DTI for short, is a simple calculation that compares your total monthly debt payments to your gross (pre-tax) monthly income. It’s usually expressed as a percentage. A high debt-to-income ratio is one of the biggest red flags that lenders look for when considering a loan application. This number measures how much debt you have compared to your income. If this ratio is too high, you may not be approved for a loan, or you could end up with a high interest rate.

To find your DTI, add up all your monthly debts (such as car loans, student loans, and credit card payments) and divide the total by your gross monthly income. For example: if you have $2,000 in debt payments each month and you make $5,000 per month before taxes, then your DTI would be 40%.

Your DTI is important because it shows Physician Bank how much of your available income is already spoken for. If we see that a high percentage of it is already going towards debt payments, we may be less likely to approve your loan request. A DTI below 45% is seen as more desirable by Physician Bank because it indicates that you have more money available each month to make your new loan payment.

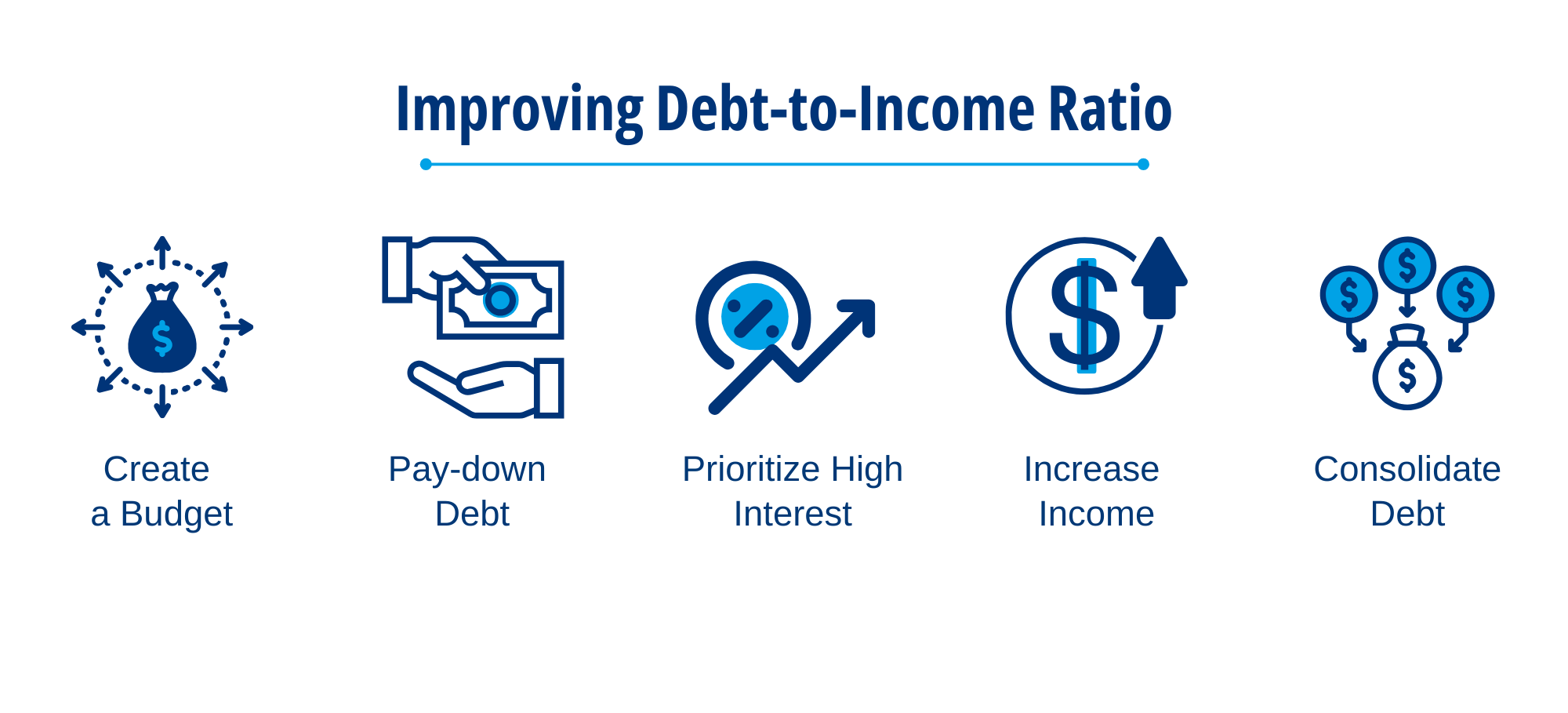

Now that you know how to calculate your debt-to-income ratio, here are some tips for improving it:

Ten Tips For Improving Your Debt-to-Income Ratio

- Make a budget: Start by tracking your income and expenses over the course of a few months. This will give you an idea of where your money is going each month and help you create a realistic budget.

- Pay down debt: Pay down high-interest debts, such as credit card balances. This will help reduce the amount of interest you pay and can significantly reduce your monthly payments. If possible, focus on reducing the most expensive debt first as this will have the biggest impact on your debt-to-income ratio. The goal should be to lower your monthly payments and save money in interest costs over time.

- Prioritize high-interest rate loans: High-interest rate loans are typically the most expensive forms of debt and can quickly spiral out of control if left unchecked. Consider prioritizing these loans above others when making payments each month.

- Increase income: Increasing your monthly income is one of the best ways to reduce debt quickly. Consider working overtime, taking on a side hustle, or negotiating for a raise at your current job. This will give you additional funds that can be used to pay down existing debts and make it less likely for Physician Bank to reject your loan application due to a high DTI ratio.

- Refinance loans: If you have a high-interest rate loan, consider refinancing them into a lower-rate loan with a longer repayment period. This will help spread out the payments and save money in interest costs over time.

- Make extra payments: Aim to pay more than the minimum each month and use any extra funds available to make additional loan payments whenever possible. This can help reduce your total debt faster and improve your debt-to-income ratio quicker.

- Consolidate debt: Consider consolidating multiple loans into one with a lower interest rate or longer repayment period. This can help lower the total amount of debt you owe each month, improve your DTI and help you manage loans more effectively. However, it’s important to choose the right consolidation loan with a lower interest rate and longer repayment period.

- Take advantage of a physician loan: Physician loans are specifically designed for doctors that have high student debt or other liabilities. These loans offer lower down payment requirements and often come with no origination fees or other hidden costs, making them attractive options for those looking to purchase a home.

- Consider physician loan forgiveness programs: If you’re struggling to pay off your medical school debt, consider taking part in one of the many physician loan forgiveness programs offered by state governments and nonprofit organizations.

- Talk to a financial advisor: A qualified financial advisor can help you create a debt reduction plan tailored to your individual needs and goals. They can also provide valuable advice on how to save money in the long-term and build wealth.

Introduction to Debt-to-Income Ratio for Mortgages

Debt-to-Income (DTI) ratio is a crucial aspect of the mortgage application process, representing the percentage of a borrower’s monthly income that goes towards paying debts. Understanding DTI is essential for both lenders and borrowers when assessing the borrower’s financial capacity to manage additional debt through a mortgage.

Key Points to Grasp When Learning About Debt-to-Income Ration for Mortgages:

· Definition: DTI is calculated by dividing the borrower’s total monthly debt payments by their gross monthly income. It is typically expressed as two ratios: front-end DTI, which includes housing-related expenses only, and back-end DTI, which incorporates all debts.

· Significance: Lenders use DTI to evaluate a borrower’s ability to handle mortgage payments alongside existing debts. A lower DTI ratio indicates that the borrower has more disposable income available to cover mortgage payments, making them a lower financial risk.

· Thresholds: Different loan programs have varying DTI ratio requirements. Conventional loans often have a maximum DTI ratio of 43%, while FHA loans may accept higher ratios. Striving for a DTI ratio below the recommended thresholds can increase the likelihood of mortgage approval.

· Impact on Approval: DTI plays a critical role in the mortgage approval process. Lenders prefer borrowers with lower DTI ratios as they demonstrate financial stability and a reduced risk of default. Understanding and managing DTI effectively can strengthen a borrower’s mortgage application.

Calculating Your Debt-to-Income Ratio

Understanding your Debt-to-Income (DTI) ratio is crucial when applying for a mortgage. To calculate your DTI ratio, follow these steps:

1. Total Monthly Debt Payments: Add up all your monthly debt obligations. Include payments for credit cards, loans, car payments, child support, alimony, and any other regular debt obligations.

2. Gross Monthly Income: Determine your gross monthly income. This includes your salary, wages, bonuses, alimony, child support, investment income, and any other source of income before taxes.

3. DTI Calculation: Divide your total monthly debt payments by your gross monthly income. Multiply the result by 100 to get a percentage. This percentage is your DTI ratio.

4. Interpreting Your DTI Ratio:

- Ideal Ratio: Lenders prefer a DTI ratio below 43%. A lower ratio indicates that you have more income available to cover your debts.

- Higher DTI Ratio: A high DTI ratio indicates that you may have difficulty managing additional debt. Lenders might see you as a higher risk borrower.

5. Front-End and Back-End DTI Ratios:

- Front-End Ratio: Compares your housing expenses to your income. It should ideally be below 28%.

- Back-End Ratio: Considers all your debts, not just housing expenses. It should ideally be below 36%.

6. Importance for Mortgage Approval: Lenders consider your DTI ratio when assessing your mortgage application. A lower DTI ratio can increase your chances of approval and potentially qualify you for better interest rates.

Importance of Debt-to-Income Ratio in Mortgage Approval

· DTI is a crucial factor in determining a borrower’s eligibility for a mortgage. Lenders use this ratio to assess an individual’s ability to manage monthly payments comfortably.

· Low DTI ratios indicate that a borrower has a manageable level of debt compared to their income, making them a lower risk for lenders.

· Lenders typically prefer borrowers with a DTI of 43% or lower, as it suggests they have sufficient income to cover their debt obligations.

· A high DTI, conversely, may signal financial strain and lead to a mortgage application being denied.

· By calculating DTI, lenders can evaluate an individual’s financial health and make informed decisions about mortgage approvals.

· Understanding and managing DTI is essential for prospective homebuyers to increase their chances of getting approved for a mortgage.

· Improving DTI by paying off debts or increasing income can positively impact a borrower’s mortgage application.

· Overall, DTI plays a significant role in the mortgage approval process and is a key metric that borrowers should consider when applying for a home loan.

Understanding Front-End Debt-to-Income Ratios

Front-end DTI, also known as the housing ratio, is crucial in determining an individual’s overall debt-to-income ratio. It specifically looks at the percentage of income that goes towards housing-related expenses. Here are some key points to understand about Front-End DTI:

· Definition: Front-end DTI focuses solely on housing costs, including mortgage payments, property taxes, and homeowners insurance.

Understanding and improving your debt-to-income ratio is an important step when applying for any kind of loan, especially physician home loans. By following the tips above, you’ll be in a better position to get approved and find the best interest rates available. If you have any additional questions about your dept-to-income ratio, please reach out to a Physician Bank loan originator.

Are you a physician in need of a loan? Physician Bank was made for you!

Start a conversation with us today.

Comments are closed