Table of Contents

Are you feeling confused by all the acronyms that come with mortgages? Let us break down one of the most misunderstood aspects of a mortgage: private mortgage insurance (PMI). This is different from your homeowner’s insurance which covers your property and belongings. PMI is insurance that protects the lender or investor from losses in the event of foreclosure. PMI is beneficial for both the borrower and the lender. For borrowers, it can help them get approved for a mortgage they may not have been able to qualify for otherwise. And for lenders, it helps protect their investment in case of a default.

Who Pays For PMI?

If you have a low down payment amount, you typically will be required to pay a PMI premium to the lender. This will typically be paid with your monthly mortgage payment. Monthly payments will continue until the principal balance on your loan reaches 78% of the original appraised value of your home (if your payments are current). At this point, your PMI will be automatically canceled. You can request cancellation earlier if you have a good payment record and your loan balance is less than 80% of the original loan amount. Property appreciation (as documented by a lender appraisal) may also help you end PMI payments sooner. It’s important to keep track of your loan balance and make sure you’re meeting any cancellation requirements.

How Much Is PMI?

PMI is calculated as a percentage of the original loan amount each year. The percentage you’ll pay varies depending on your credit score, the size of the loan, and the down payment amount. It typically ranges between 0.5% and 2%. This amount is set at the start of your loan and may not decrease over time.

How Can I Avoid PMI?

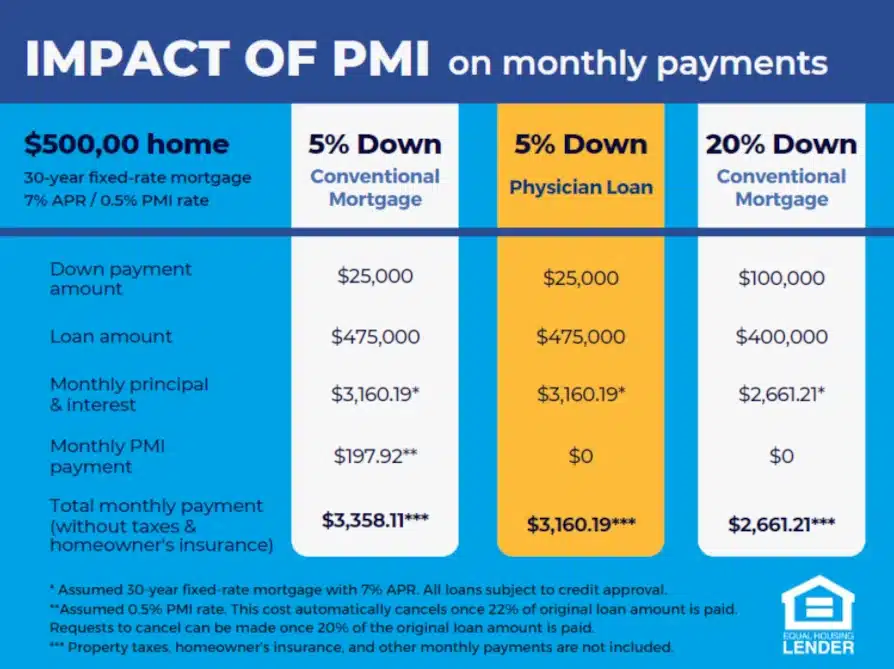

With many home loans – like a conventional mortgage – it is recommended to have a down payment of 20% or more of the property’s value to avoid paying for PMI. You can still avoid PMI monthly payments if you can’t afford a 20% down payment. Physician Mortgage Loans through Physician Bank do not require qualified borrowers to pay PMI, even if the down payment is less than 20%. Let’s break down the impact PMI has on monthly mortgage payments for a 30-year fixed-rate mortgage on a $500,000 home, assuming a 7% annual percentage rate (APR) and 0.5% PMI:

In this scenario, if your down payment is 5%, you will save almost $200 a month with a physician loan.

Can I Avoid PMI With a FHA Loan?

Mortgages backed by the Federal Housing Administration (FHA) can be a good option for borrowers with low down payment funds and lower credit scores. There is no PMI with an FHA mortgage, but they do often require a mortgage insurance premium (MIP) that extends for the life of the loan and can’t be canceled.

Private mortgage insurance is a requirement for many borrowers, but physician loan borrowers do not pay mortgage insurance. If you are a qualifying physician and are interested in purchasing a home, apply today with Physician Bank or call us at (888) 632-2651. We would be happy to help you get into the home of your dreams without added expenses like private mortgage insurance.

Physician Bank is an Equal Housing Lender, Member FDIC, and a division of Heritage Bank NA. All loans subject to credit approval.

Are you a physician in need of a loan? Physician Bank was made for you!

Start a conversation with us today.

Comments are closed